Updated – 23/3/2022 – Added map for ‘Customs Site No.1 Solent’ at Marchwood, revised Fawley Waterside to reflect newly published Solent Freeport brochure.

Introduction

Two years have passed since HM Government announced the Freeport Consultation. Since that time, the eight shortlisted Freeport teams still in competition for Treasury funding have kept their cards close to their chests. With the current deadline for submission of its Full Business Case just a few weeks away, the Solent Freeport website is still short on detail.

There is, however, one detailed source of information that has been made available in the public domain in advance of the business case detail. HMRC published five out of the six detailed Solent Freeport tax site maps on February 22nd 2022. This SPS discussion paper provides links to the detail in those maps and in the absence of any further information, highlights a few of the conclusions that might be drawn.

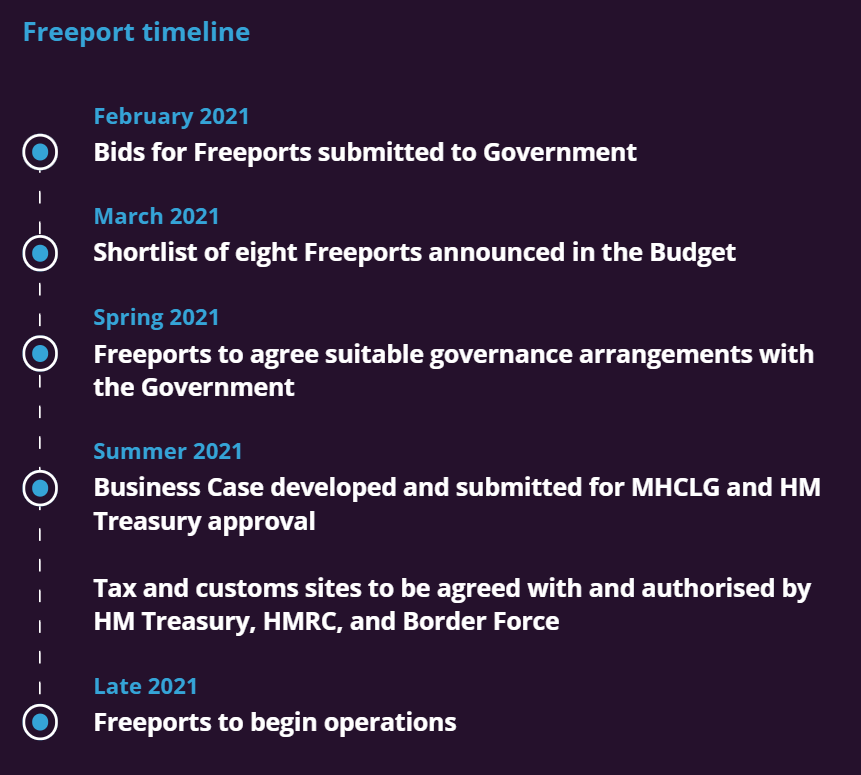

Both the UK Government and Solent Freeport websites still show that the first Freeport “will be operational in late 2021”, an indication that the programme is already running rather late. If it is to progress to the stage at which contracts are placed, far more detail is needed.

This paper, which is intended to invite discussion, is set out as follows:

Solent Freeport Outer Boundary

Redbridge / DP World

Marchwood Port / ABP ‘Strategic Land Reserve’

Fawley Complex

Fawley Waterside

Navigator Quarter

Dunsbury Park

Solent Freeport delivery phasing

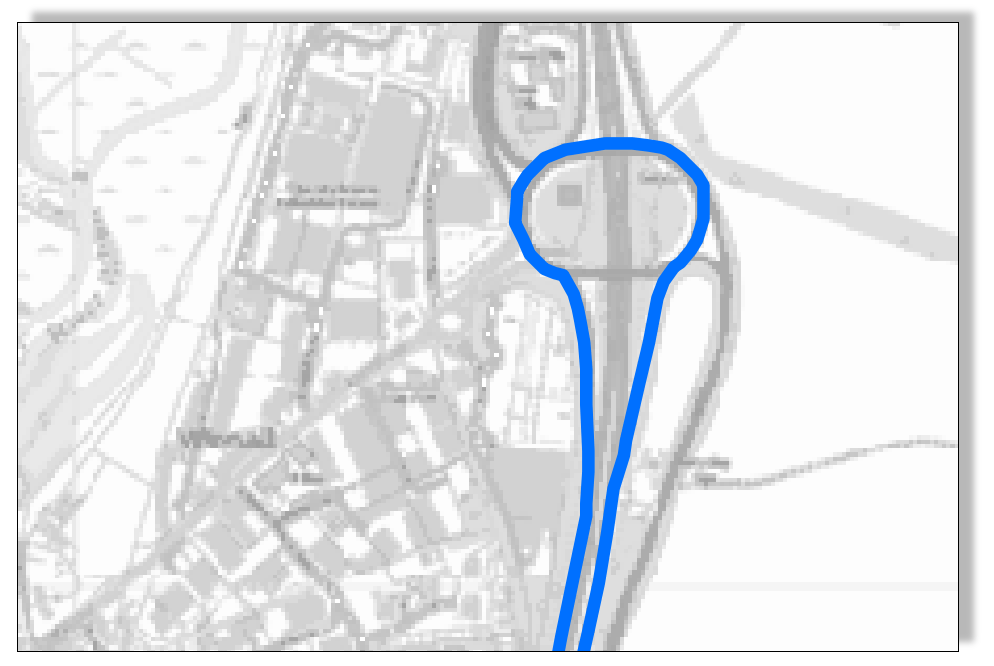

Solent Freeport Outer Boundary

The Outer Boundary map shows the geographical boundary within which the UK Treasury and HMRC freeport rules and regulations will apply. It would appear that the strict 45 Km ‘Outer Boundary’ rule originally written into the bid prospectus (at page 16) has been revisited. The boundary shown by the blue line in the recently published map simply follows the boundaries of the local authorities involved but with a curious north-bound extension following the M3 carriageways up to and around the Winnall Interchange:

Is this simply an ‘escape route’ for trucks which inadvertently exit the boundary or is this, perhaps, an opportunity for a future scope extension to bring in the Winnall employment sites?

Click on the image below and the (very large) full size map will open as a PDF document that you can drag and zoom with your mouse, or pinch and zoom with your finger, depending on your device. As you zoom into the map, you’ll also see the defined boundaries of the six designated tax sites.

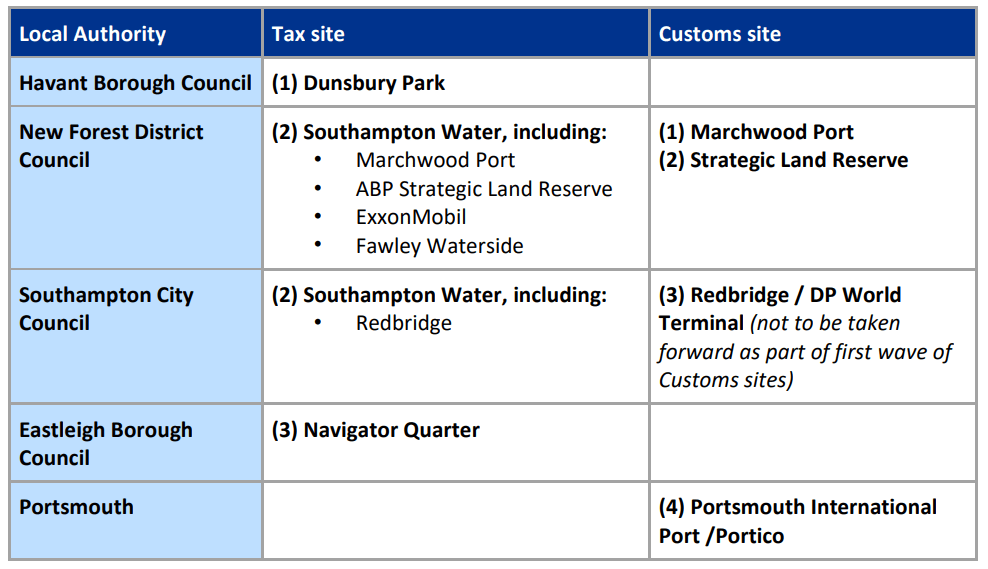

In addition to the freeport tax sites but not shown on that map, there are four defined freeport customs sites, listed alongside the tax sites in the table below:

The following graphic shows the six tax sites now defined by HMRC, mostly concentrated around Southampton Water with a further site adjacent to Southampton Airport and one much further to the east alongside the A3(M) between Waterlooville and Havant.

The sections below provide links to the detailed maps for each of the six tax sites and raise some possible discussion points in advance of any official detail on their proposed use. In each section, click on the map image and the official HMRC boundary map will open in a new browser session. Note that these are large maps and you can zoom in and pan around to see the full detail.

The tax sites are given one of three classifications in this post – ‘Existing Facility’, ‘Brownfield’ or ‘Greenfield’ – classifications which aid speculation on the possible delivery ‘waves’ within the Solent Freeport delivery programme. Under each tax site heading, the most likely aligned customs site(s) are also shown.

Now that the freeport tax site maps have been released, it is surprising to find that the Vestas site at Newport, Isle of Wight, has not been included in the freeport definition. In a previous website post, SPS pointed out that the original Solent Local Enterprise Partnership (LEP) freeport consultation response highlighted that the Vestas workforce of 1,200 at Newport IOW were “at significant risk of being relocated offshore due to potential tariff increases as a result of Brexit”. That statement was interpreted as suggesting that a tax site could be defined on the Isle of Wight, however from tax sites now announced, there is nothing in the proposal to mitigate that risk.

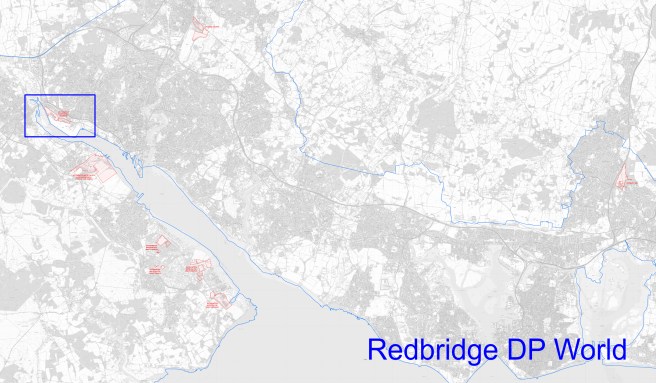

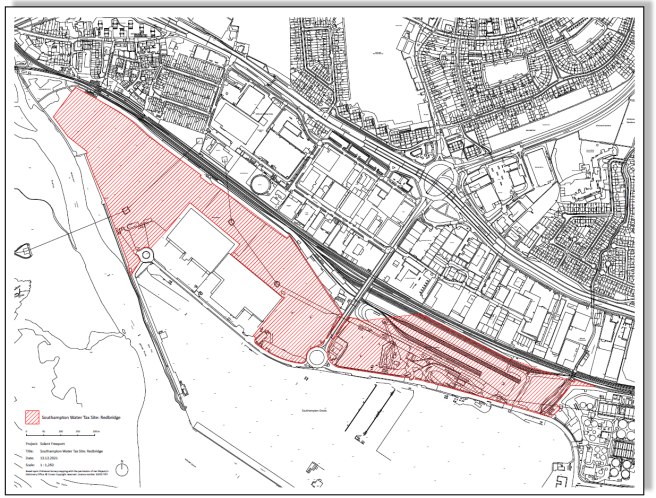

Redbridge / DP World – DP World

Tax site – Existing Facility

Customs Site – Redbridge / DP World

Assumed programme delivery priority – Medium

The table above noted that the Redbridge / DP World customs site is “not to be taken forward as part of first wave of Customs sites”, indicating that while this facility has been defined and documented as required by the bid process, it is reserved, probably along with this tax site, for implementation as part of a second or subsequent Solent Freeport delivery ‘wave’.

Scheduling the Redbridge / DP World tax site to a future phase would give the DP World port management more time to assess any possible risk to ‘non-freeport’ trade that might be associated with ‘switching on’ freeport status at the facility. The current use of the land within this tax site boundary is for car parking and the storage of vehicles as freight.

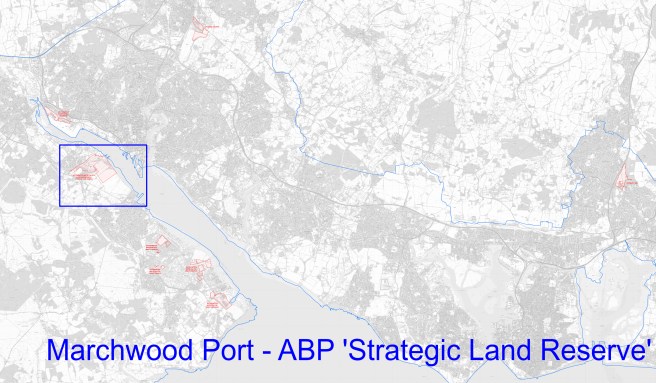

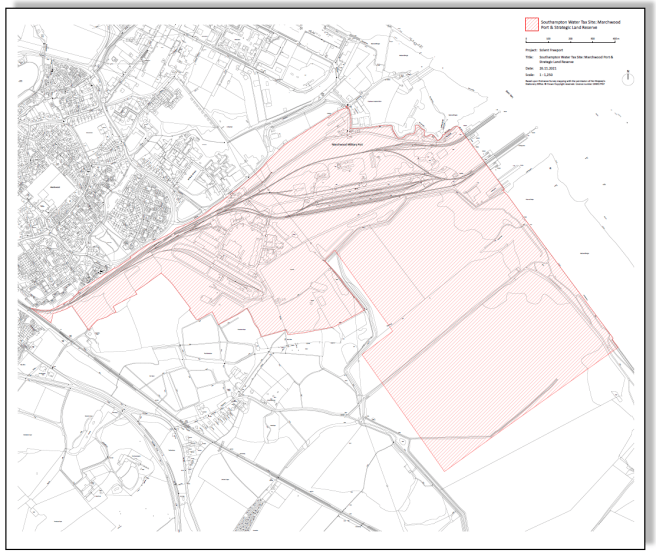

Marchwood Port / ‘Strategic Land Reserve’ – Solent Gateway / ABP

Tax site type – Existing Facility / Greenfield

Customs Site – Marchwood Port / ABP ‘Strategic Land Reserve’

Assumed programme delivery priority – High/Medium

It is notable that ABP have only submitted the northern part of their Dibden Bay ‘Strategic Land Reserve’ for definition as a freeport tax site. Leaving the southern part of the Dibden Bay site out of the freeport definition enables ABP to retain an option to keep this part of the ‘Strategic Land Reserve’ for future expansion of its non-freeport operations from the eastern shore.

Current environmental regulations give the Dibden Bay shoreline some level of protection from development, however once the freeport is in operation, developments within its boundary will benefit from the government’s proposed relaxation of planning regulations within freeports. As SPS observed in our report from May 2021, the Solent LEP at page 17 of their consultation response suggested that permitted development rights in freeports should be extended to enable those rights to supersede existing environmental development regulations.

Once development of the northern part of the Dibden Bay shoreline has been permitted under the freeport rules, then a precedent would have been set which could then be used to attempt to override the existing environmental protections outside the freeport boundary in the southern part of the ABP ‘Strategic Land Reserve’.

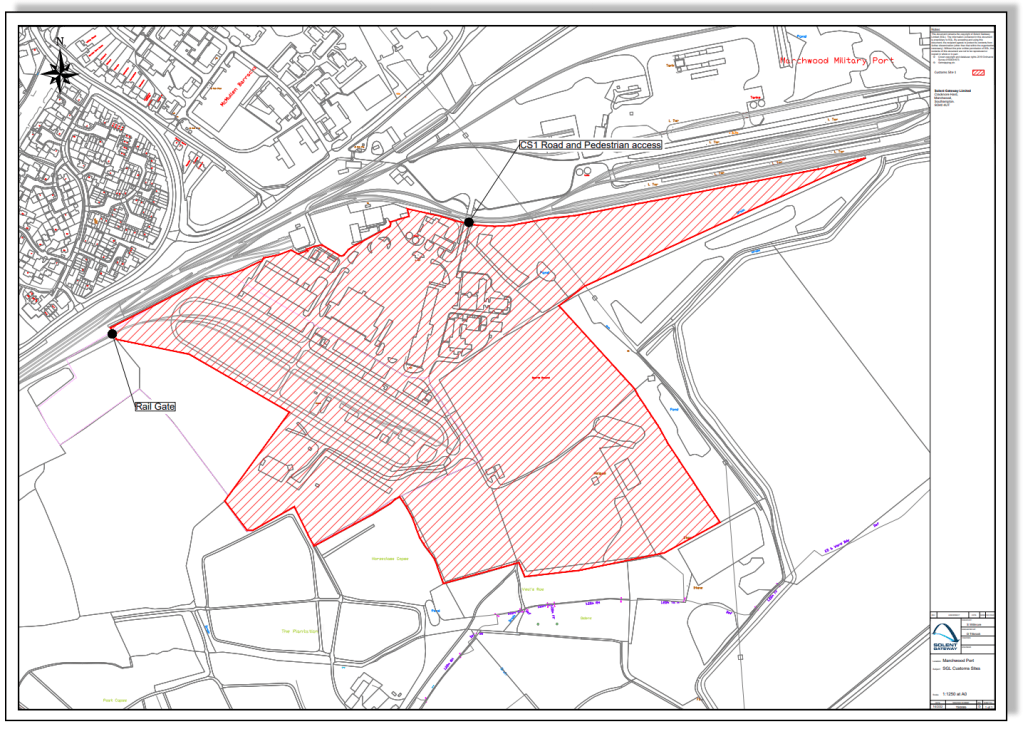

‘Customs Site No. 1 Solent’ (Solent Gateway Ltd.)

Published 17th March, this map shows ‘Customs Site No.1 Solent’, situated within the Solent Gateway Marchwood Port tax site:

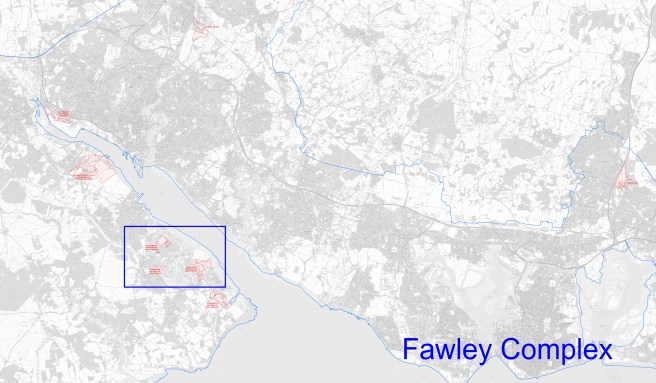

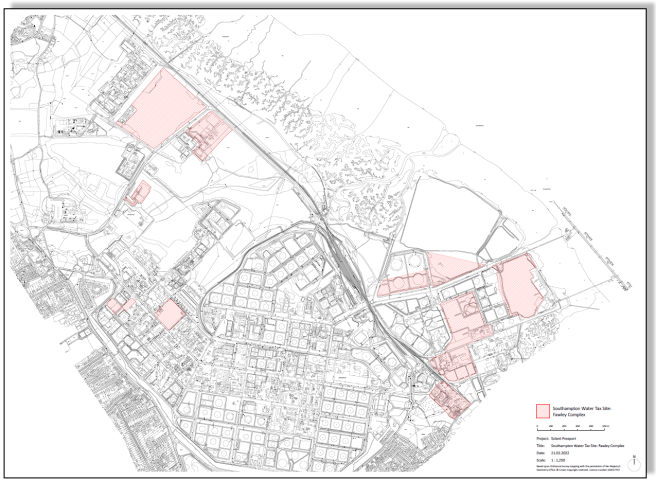

Fawley Complex (ExxonMobil)

Tax site – Brownfield

Customs Site – Marchwood Port / ABP ‘Strategic Land Reserve’

Assumed programme delivery priority – Low

The tax site boundaries within the existing Fawley complex define about a dozen specific areas visible if you drill into the detail of the map. These are probably simply a defined set of ‘brownfield sub-sites’ within the ExxonMobil perimeter that would be available for redevelopment as required. By speculatively defining those otherwise unmarketable individual areas as tax sites, the owner of the site is potentially keeping options open should the freeport prove successful.

For now, freeport developments at this site would appear to have low schedule priority.

Fawley Waterside

Tax site – Brownfield

Customs site – Marchwood Port / ABP ‘Strategic Land Reserve’

Assumed programme delivery priority – High

This is one of the more intriguing of the recently announced freeport tax sites. Owned by Cadland Estates, whose current planning application shows the rather imaginative development plan which SPS has been following for a while, it seems that the management team might now be looking to the freeport opportunity to provide a more immediate commercial return. With much of the Fawley Waterside site now included in the tax site boundary, it looks as if the current proposal for the site could change if the Solent Freeport Full Business Case is approved.

Last year, when questioned about the selection of the tax sites, the Chairman of the Solent Freeport Board, Brian Johnson, remarked that “Fawley Waterside has huge potential”, a comment which given the current plan for the Waterside site was interpreted at the time as being a reference to potential development to the north in Dibden Bay.

The latest marketing brochure just issued by Solent Freeport shows the site as a “net zero smart town development, an intelligent merchant city surrounded by parkland, facing the Solent waterfront and backing on to the New Forest National Park” including “1500 residential units alongside 125,000 m2 of industrial space, 50,000 m2 of office space and associated retail, civic facilities, a school, a hotel and a marina”. The same brochure also states that “Outline planning permission was granted in 2020 and investors and tenants are now being sought for the first completions in 2023”. This is perhaps a little premature given that as of March 2022 the planning application is still showing as ‘Awaiting decision’ on the NFDC planning portal.

It is not clear how that land use now aligns with its new tax site status and until the site’s ‘huge potential’ is explained by publicly visible detail in the Full Business Case, that unanswered question leaves the way open for further speculation.

What follows is just that, a speculative hypothesis by this author.

With no freeport tax site defined on the Isle of Wight, the ‘significant risk’ to the future of the Vestas Newport workforce, already highlighted by the Solent LEP, may now have increased in likelihood.

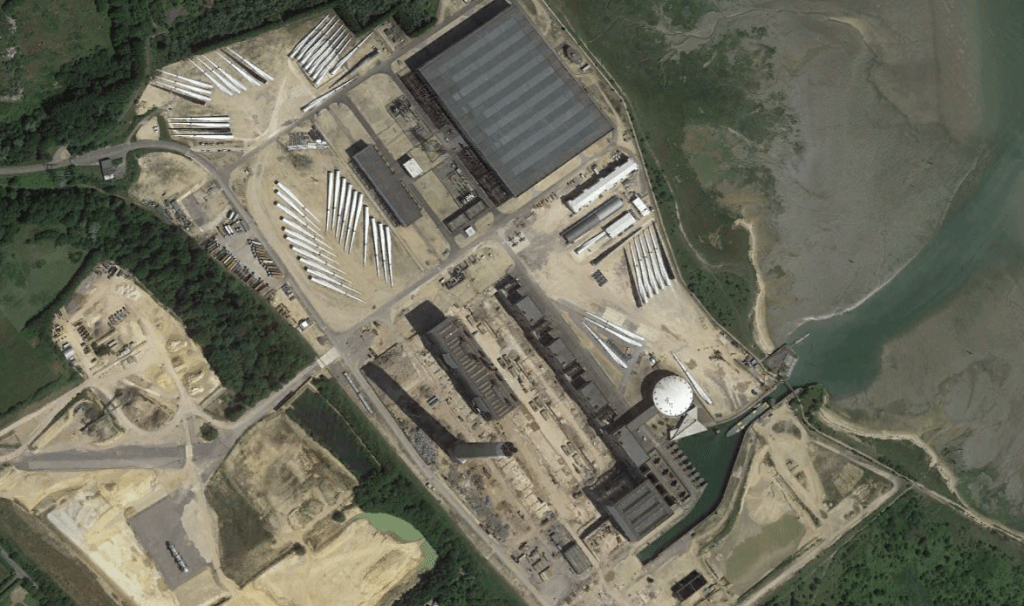

Vestas, a Danish based global corporation, now manufactures generators, blades, pylon components and control systems in facilities in many regions, including both Europe and the Far East. Coincidently, they have also been using the Fawley site for storage of blades for some years, as witnessed by the aerial image below, showing ‘Bladerunner’ in the power station dock.

With a little lateral thought, a significant part of the Fawley Waterside site could now be re-developed for Vestas as a transit site for the consolidation and forwarding of complete sustainable wind energy systems, using components brought in from different geographies, turbine blades, generators, nacelles and tower components, benefitting from value-added system assembly on the Fawley Waterside site under freeport tax rules.

Taking this proposition to a further stage, there might be further commercial advantages for the delivery of such systems directly for installation at offshore sites outside national tax boundaries.

Once the business case is visible, the ‘huge’ value represented by the ‘intelligent merchant city’ proposition will doubtless become clear. Until then, and until there is clarity on just how and when the Solent Freeport will deliver the benefits promised, speculation will continue.

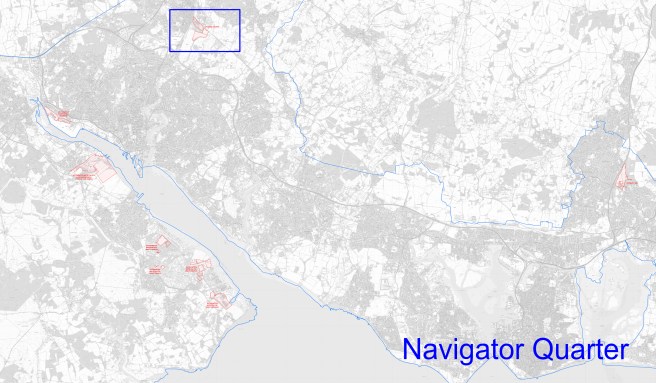

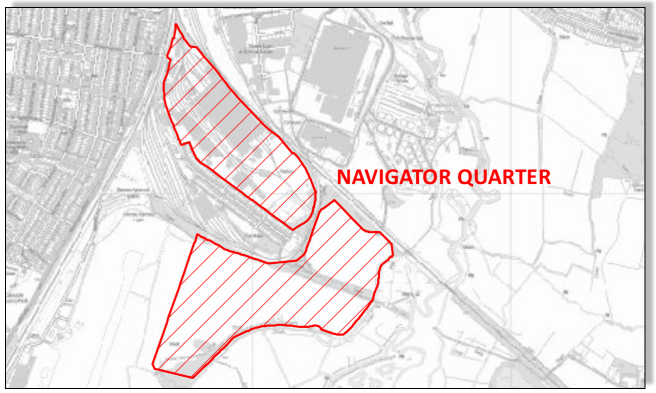

Navigator Quarter

Tax site – Brownfield / Greenfield

Customs Site – Marchwood Port / ABP ‘Strategic Land Reserve’ / Redbridge DP World

Delivery priority – Low

The detailed map of the ‘Navigator Quarter’ tax site has not yet been published by HMRC, but its boundaries can be viewed in the image above. The northern part of the site is ‘brownfield’, re-using the former Eastleigh Works rail site at the northern end of Southampton Airport’s runway. The southern part of the tax site occupies ‘greenfield’ space linking the Eastleigh Works directly to the eastern perimeter of the airport.

The absence of a freeport customs site defined for Southampton Airport is surprising, but presumably reflects the current limited range and access of flights to appropriate overseas facilities. This may change in the future once the current runway extension project enters construction. For now, development of at least part of the Navigator Quarter tax site could be dependent on the runway extension schedule, although the remainder of the site could also provide separate storage and manufacturing space within easy controlled motorway reach of Redbridge, 7.7 miles to the south west.

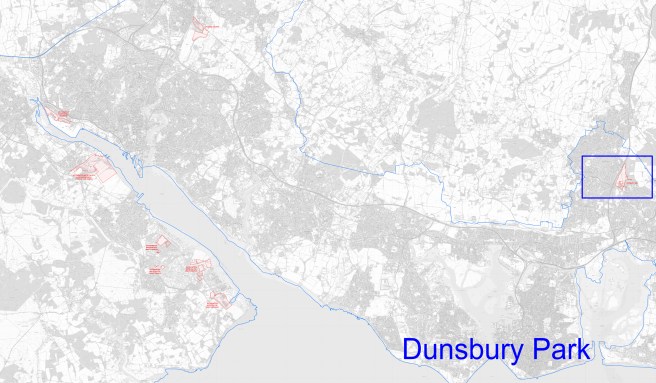

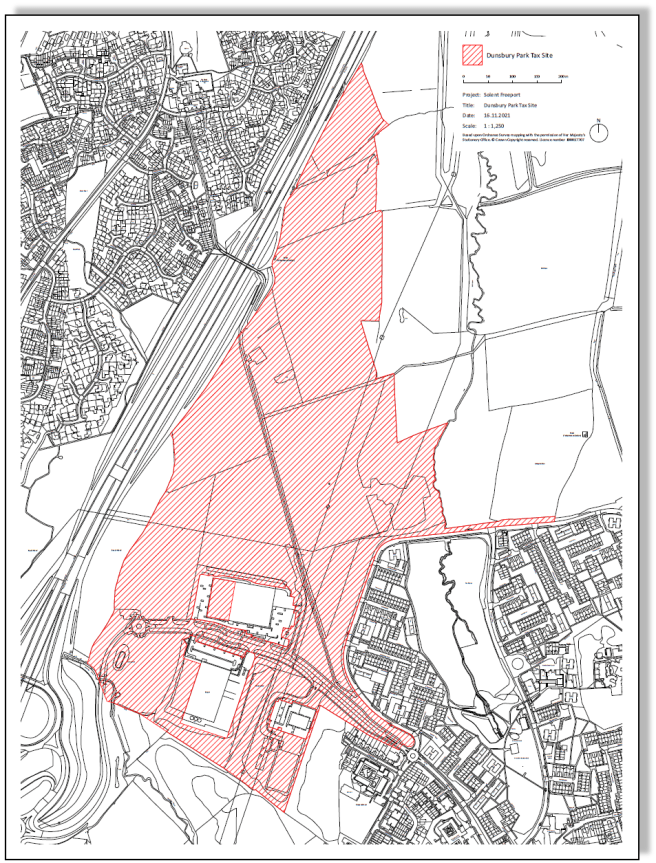

Dunsbury Park

Tax site – Existing Facility / Greenfield

Customs Site – Portsmouth International Port

Assumed programme delivery priority – Low

Dunsbury Park is a relatively new greenfield employment area to the west of Havant. In common with Portsmouth International Port (PIP) and Portico Shipping, the small commercial port operation within PIP, the site is wholly owned by Portsmouth City Council. Havant Borough Council’s sole financial interest here is as the local authority for business rates purposes.

Situated 30 miles from the nearest Southampton Water customs and tax sites, Dunsbury Park would probably be exclusively related to the freeport customs site sited at Portsmouth International Port, 8.5 miles away. Given the lack of available dockside space at the Portsmouth site, it seems likely that the Dunsbury Park site would be used to provide offsite secure warehouse space for Portico.

Portsmouth City Council’s publicly stated priority is to upgrade passenger terminal facilities to support an expanded cruise ship operation. Without any obvious short term plans to expand the commercial activity at the port and given the relatively small scale of commercial shipping currently using the port, the Portsmouth/Havant freeport sites are unlikely to take high priority in an early Solent Freeport programme delivery wave.

There is another intriguing possibility based on commonly observed use for freeports. While commercial shipping may be low volume traffic at Portsmouth, an increasing number of yachts owned by the mega-rich can be seen visiting the harbour these days and the Dunsbury Way site could provide the secure warehouse home to some notable – but invisible – private collections.

Assignment of freeport tax status to a site may have the effect of preventing it’s use for any other ‘non-freeport’ purpose, a cautionary note which might suggest a reason why only half of the Dibden Bay site was allocated as a tax site. In the case of Dunsbury Park, however, the entire site has been defined as a tax site. This would potentially ‘mothball’ the employment site until such time as the Portsmouth component of the freeport programme is up and running.

When the PCC Leader celebrated the legal agreement giving Dunsbury Park special tax status through the Solent Freeport, his finance director, Chris Ward, warned that the agreement, which puts ‘onerous’ conditions on the council, is ‘likely to limit the type of tenant we can attract to Dunsbury Park‘. A cabinet report noted that the agreement ‘does complicate matters in creating significant levels of uncertainty in governance, financial and market impact and legal obligations‘, but adds: ‘This may well be an acceptable sacrifice given the wider benefits of freeport status across the region‘.

If the eastern end of the Solent Freeport remains dormant until a second or third wave of the delivery programme, then Havant Borough Council, depending heavily on the jobs they believe the freeport will bring, may not be quite as agreeable that this is ‘an acceptable sacrifice‘.

The Havant Borough Council Cabinet paper referenced above, also contains a note of caution for any local authority which hosts a Solent Freeport Tax Site. It is important for all levels of the Council, both officers and elected representatives, to understand that Business Rates levied on new developments within the tax site boundaries are not retained by the local authority concerned, but are pooled at the overall Solent Freeport level for use across all parts of the programme. Some of the common spend will end up back in the source local authority but the basic principal to be agreed is that no council should be worse off as a result of freeport implementation. Local authorities should set their expectations for financial income accordingly realistically.

Note: An explanation of this was given by Solent Freeport staff and KPMG consultants to the HBC meeting, see recording link under ‘Sources’, below.

Solent Freeport Delivery Phasing

The Solent Freeport website and the UK.Gov site both still present timelines showing the first freeport becoming operational in ‘Late 2021’.

The freeport programme therefore already shows clear signs of delay, a trend that can be expected to continue given the complexity of the full programme, its supporting legislation, the process of placing contracts and the myriad of dependencies.

Quoting from the Havant Borough Council Cabinet Paper, “The Full Business Case is currently in a draft form and due to be submitted to Government by 15th April 2022. The primary purpose of the FBC is to ensure that prospective Freeports have duly considered all of the factors critical to successful delivery of a Freeport. However, it is also the mechanism through which prospective Freeports must provide final assurance to the Government that public funds granted to the Freeport will be effectively managed.”

The evidence from the maps, combined with many years of experience of complex programme delivery, might suggest the following delivery phases, with the four customs sites implemented in three waves. This timeline, of course, already starts sometime after 15th April 2022 when the Full Business Case has been approved.

Disclaimer

Adding firm dates to any event beyond the submission of the Full Business Case in April 2022 is, of course, impossible without detailed understanding of the Solent Freeport delivery programme. In the absence of any publicly available detail, this is simply speculation by the author, informed only by the content of the maps and previously available documentation relating to the freeport bid process.

This is a major programme of work that could have far reaching consequences across the Solent area. Solent Protection Society look forward to reviewing further detail from the Solent Freeport programme with interest.

Sources:

UK Government Publications – Solent Freeport tax sites

UK Government Publications – UK Freeport Maps

Havant Borough Council Cabinet paper – March 7, 2022

Havant Borough Council Cabinet meeting – March 7, 2022 (recording)

Portsmouth News – February 9, 2022

Previous SPS Articles on this subject

Post author: Bob Comlay – SPS Council Member

For details of how to become a member of Solent Protection Society, please take this link and get in touch.

If you are passionate and enthusiastic about the preservation of the Solent and would like to add value to the SPS Council through your knowledge of:

Pollution

Climate Change Adaptation

Planning and Development

Marine Science and Conservation

Web & Social Media Publishing

Please contact our secretary in the first place – secretary@solentprotection.org