In the last budget, the Solent was shortlisted as the site for one of ten Freeports to be set up in the United Kingdom. Since that time, we’ve seen little or no detail in the public domain regarding what the Freeport opportunity could mean for the Solent region.

In this article, we try firstly to summarise the ‘Bidding’ process used to arrive at the Budget Statement, and secondly to summarise what a ‘Solent Freeport’ might mean to our area. There are two relevant documents referenced, both are viewable as PDF files by clicking the two images below. Each document will open in a separate browser tab and you may wish to refer to them as you continue to read this article.

The first document, the ‘Bidding Prospectus’ for the work, sets out the government’s ambition for Freeports, the government’s core Freeport objectives, what was expected of bidders and what a best-in-class Freeport proposal should set out. The document includes the prescriptive format in which the response must be written, and explains the marking scheme by which competing bids will be judged. The document provides additional detail on the UK’s Freeports model, including clear geographic guidelines on site design and size, and how Freeport levers relating to customs, tax, planning, regeneration and innovation will work.

The ‘Response’ by the Solent Local Enterprise Partnership (LEP) covers all points in the required format, while identifying differentiators unique to the Solent – i.e. selling the reasons why the reviewer should choose this proposal.

The “Bidding Prospectus”

The stated objectives for these freeports are to become “national hubs for global trade and investment across the UK“, to “promote regeneration and job creation” and to “create hotbeds for innovation“.

In this article, using the government’s Freeport Bidding Prospectus as our source, we look first at the government’s brief for a UK Freeport model showing how it might apply geographically to a Solent Freeport. We then look at the conceptual examples of possible solutions given by the Government – or more likely by their ‘special advisors’, a term which may engender caution – using words lifted straight from the government’s tender document. Lastly, we raise a few concerns about the impact that the development of a Solent Freeport could have on the environment of the Solent.

Understanding the ‘Freeport’ concept

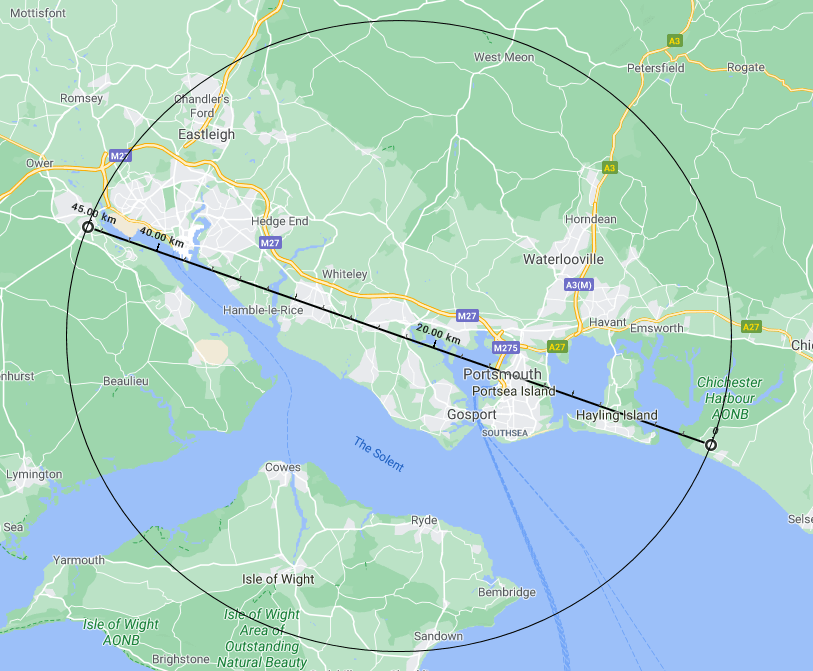

The UK Government document sets out the overall scale of a Freeport and demonstrates for a ‘multi-port’ model how the maximum outer boundary could fit with the local geography of the port facilities, regeneration sites, existing storage facilities and the motorway infrastructure that services them.

The proposed model allows for multiple sites to be designated within the overall Freeport. In the case of the Solent Freeport, this could allow for collaboration between ports, businesses, wider stakeholders and relevant economic assets across the various local authorities and port authorities by allowing them to benefit and contribute to one Freeport in their region. The model also ensures that businesses looking to invest in Freeports have increased options available to help them secure an optimal location that works for them. This could be considered as shorthand for changes to the Planning System processes for Local Development Orders and the relaxation of permitted development rights within the Freeport outer boundary.

The bidders were required to “set out on a map the area where they propose the Freeport tax measures should apply in compliance with the government’s requirements”. This presumably is in an appendix to the Solent LEP response still deemed ‘commercially sensitive’ since it’s not yet been made public. Since the furthest permitted distance between any two sites within the same Freeport is 45km and the largest area a Freeport Outer Boundary can cover is a circle of diameter 45km, it’s not hard to draw a map which addresses the requirement.

The ‘Solent Freeport’ in a geographical context

The Solent Freeport would be an area designated by the government where companies associated with the freeport have distinct tax advantages. Companies that operate within freeports don’t have to pay import taxes (tariffs) on products until they move them outside the outer boundary and into the full UK market. They can avoid paying certain taxes altogether if they bring in goods through the ports and airports to store or manufacture on sites within the circle before they export them again.

In the case of the Solent Freeport, this could allow for collaboration between the port areas on both sides of Southampton Water, those within Portsmouth Harbour and those on the north coast of the Isle of Wight. There are also intriguing opportunities for the smaller ports and harbours scattered around the Solent shore, within the ‘magic circle’. Since the northern part of the IoW and parts of Portsmouth already benefit from UK Assisted Area status, the definition of Freeport status would provide further incentive to businesses to locate and expand in those areas.

The key to making a Freeport work across the 1,500 square kilometres is in the strict control of movement of products between the various sites – factories, warehousing, customs points and port areas – using RFID technology and ANPR cameras. While the underlying technologies are well known, RFID tags to control inventory movements in shops and warehouses and ANPR cameras to manage speeding on motorways, there is a significant body of evidence concerning criminal risks in freeports and factors that give rise to those risks. Like other freeports across the world, the new UK freeports could also be used to store – without tax – high-value goods, including art, precious metals and fine wine. Such tax-free perks have transformed some freeports into self-storage units for many of the world’s wealthiest people with Geneva’s freeport alone estimated to house over a million works of art, including 1,000 Picassos.

So how might all this affect the Solent Region?

The Solent LEP response is heavily biased towards Southampton as the major opportunity area. the city being mentioned thirty-one times against a total of five for Portsmouth and three for the Isle of Wight. However, a glance at the outer boundary map above shows the significance of all three port locations. With the extension of Southampton Airport’s runway now almost certain to go ahead, the Solent region will be better able to support inbound and outbound air freight within the Freeport outer boundary and directly alongside the M27 corridor. To the east, Portsmouth International Port is readily securable lying as it does, inland from the countries premier Royal Naval dockyard. Portsmouth itself, as the Solent LEP response notes rather pessimistically, only has three roads on and off the island on which it lies. Far from being a disadvantage, this would help to secure routing of inbound and outbound freight directly to and from the M275.

To the north east, a short direct journey via the M275 and A3(M) lies the Dunsbury Park warehousing and distribution site alongside the A3(M) between Havant and Waterlooville. Since Portsmouth City Council own both the Portsmouth International Port and the Dunsbury Park site, the city owns both port facilities and secure warehousing and distribution space within the ‘outer boundary’, linked by an easily monitored motorway link.

There are multiple other sites alongside the M27/A3(M) corridor between Havant and Southampton, all of which could host manufacturing and warehousing facilities which might benefit the Freeport model.

The southern part of the Solent Freeport outer boundary includes Newport and the Medina River, and the Solent LEP highlights another advantage of the Freeport in this event. In consideration of Vestas, the Danish global company making wind turbine blades at Newport, they note that the company and its local workforce of 1,200 are “at significant risk of being relocated offshore due to potential tariff increases as a result of Brexit”. Clearly, the tax incentives associated with the Freeport could help to mitigate that risk.

The Freeport ‘Economic Levers’

The ‘Freeport levers’ are the changes that will be made by the UK Government to streamline customs rules, tax rules and planning regulations to aid ‘regeneration’ and ‘innovation’.

While customs rules and tax rules will occupy business, the subject most likely to affect individual Solent Protection Society members is that of Planning. Changes to Local Development Orders and Permitted Development Rights are proposed at a national level in order to remove restrictions and delays for associated development within the new freeport outer boundary.

In their response, the Solent Freeport team welcomes the use of Local Development Orders (LDOs) as they “establish a clear framework for development, giving certainty to applicants, businesses and communities”. However, the process for securing an LDO is often “time intensive and requires skills that many Councils do not possess” and also “require the support of a wide range of stakeholders”. The Solent LEP response suggests that the Government improve the Local Development Order process by imposing strict time limits on their delivery. To achieve this, they suggest the establishment of service level agreements between relevant local government authorities committing to a reasonable decision period for various approvals relevant for a given site.

Given the large number of local authorities across the Solent freeport region, Solent LEP go further, proposing “the establishment of a special Virtual Planning Authority that is facilitated by a coordinating institution with the cooperation of relevant local authorities”. This is a direction which Solent Protection Society believe should be pursued with great caution. There are already well publicised proposals, for example the Aquind Interconnector project near Portsmouth and the Southern Water desalination plant near Fawley, where opportunities for public and local authority scrutiny are being overridden by central governments’ declaration of the initiative as a ‘National Infrastructure Development Project’.

The Solent LEP response also proposes “extending the permitted development rights accorded to ports to include assembly and manufacturing though they believe this would still not improve the planning environment enough to act as an incentive to potential investors. While the expansion of permitted development rights would simplify development processes on seaport land, it would still not allow for the greater freedoms or coordination in higher-level planning required to ensure Freeport success.”

In what might seem to some a worrying threat to environmental standards, the Solent LEP go further, suggesting that “existing environmental regulations along much of the UK coastline supersede Permitted Development Rights, further limiting their additional value as an incentive”.

Solent Protection Society will be keeping a close eye on the Solent Freeport programme as it develops. We are, however, mindful of the fact that Freeports are not a new idea in the UK – the country had a couple of them as recently as 2012 before the government of the day abandoned them for failing to deliver the expected benefits.

Bob Comlay

April 2021